Deep Industries Ltd. Deep Value, or Value Trap?

A company grew by 50% in FY26, yet stock price has not delivered any return. This is the paradox at the heart of Deep Industries. Today, we try to answer why.

Picture this. You stumble upon a small-cap company in the unsexy corner of India's oil and gas sector. It has quietly compounded revenues at 36% CAGR over five years. Its profits have grown at 43% CAGR over the same period. The underlying business, steady, recurring, and government-backed, has never missed a year of positive operating cash flows in eight years. And yet, the stock has delivered barely 3% return in the last twelve months, while the broader market has moved ahead.

This is not a hypothetical scenario. This is Deep Industries Limited (DIL), an Ahmedabad-based oil and gas field services company that has spent over three decades building what is arguably India's most integrated and defensible oilfield services franchise, largely out of the spotlight.

The question every investor who has looked at this name is wrestling with is simple: is this deep value, a business being fundamentally misunderstood by the market, with a re-rating waiting in the wings? Or is it a value trap, a business that looks cheap for good reason, with a string of governance concerns and execution risks that justify the market's skepticism?

That is the question this newsletter sets out to answer. But before we get there, you need to truly understand what this business does, because that understanding is the foundation of everything else.

So What Does Deep Industries Actually Do?

When oil or gas is discovered underground, the job of finding it is called exploration. That gets all the headlines. But what happens next: extracting it safely, processing it, compressing it, and transporting it, is an equally complex, capital-intensive operation. This is the world Deep Industries lives in. It doesn't explore. It doesn't refine. It doesn't sell petrol at a pump. It is the invisible plumbing that makes India's gas fields actually work.

Think of it this way. You know how the water in your building's overhead tank only flows to your tap because there is a motor that pumps it up? Without that motor, the water just sits there, unable to travel the distance or reach the height it needs to. Natural gas works the same way. When it is extracted from a well deep underground, it comes out under pressure. But as it travels through pipelines towards homes, power plants, and factories, that pressure drops over distance. Without something actively pushing it along, the gas simply stops flowing, or moves too slowly to be useful. Deep Industries provides those giant industrial "pumps," called compressors, that keep India's gas moving from wellhead to pipeline.

Now, why would ONGC or Oil India pay DIL to provide these compressors rather than simply buying them directly? The answer is the same reason you might rent furniture from Furlenco instead of buying it outright. Furlenco lets you get a Rs. 1.5 lakh sofa for a monthly rental of a few thousand rupees, without locking up capital, without worrying about maintenance, and with the flexibility to upgrade or return it as your needs change. DIL does exactly the same thing for oil and gas companies, only the "furniture" is a Rs. 15 Crore industrial compressor package that requires specialized engineers to run it round the clock. This model, where DIL supplies, installs, operates, and maintains the equipment while the client pays a fixed monthly or per-unit fee, is called charter hire, and it is the foundation on which the entire company is built.

DIL was founded in 1991 by Paras Savla and Rupesh Savla. Its first breakthrough came in 1997, when it became the first company in India to provide natural gas compressors on a charter-hire basis, a contract with ONGC at Mehsana, Gujarat. That single innovation redefined how PSUs sourced field services and gave DIL a three-decade head start on everyone else. Today, it holds 95% market share in India's outsourced onshore gas compression services.

A Word on That 95% Market Share

At first glance, 95% market share sounds like an extraordinary moat. And in some ways it is. But a careful investor should also ask the question from the other direction: if this industry is so attractive, why hasn’t anyone else tried to grab a share of it?

The honest answer is that the charter-hire gas compression market in India is real but relatively niche. Most national oil companies globally own their compression equipment in-house. India’s outsourcing of this function to the private sector is a fairly specific structural characteristic of how ONGC and Oil India have historically operated. The market is not so large that it has attracted aggressive international/domestic competition, and the barriers to entry, while real (ONGC vendor qualification takes 3 to 5 years, the equipment is specialized and imported from the US, and managing O&M in remote gas fields requires years of accumulated technical know-how), are not so towering that they would stop a well-capitalised player from entering if the prize were big enough.

What this means in practice: the gas compression business alone, while profitable, is unlikely to be a very lucrative opportunity on its own. Its value lies in the stable, recurring, high-margin cash flow it generates, which DIL has been using as a launchpad to build adjacent, significantly larger businesses. The real growth story of Deep Industries is not about dominating a niche. It is about using that niche as a beachhead to enter the PEC and offshore markets, both of which are orders of magnitude larger in addressable opportunity.

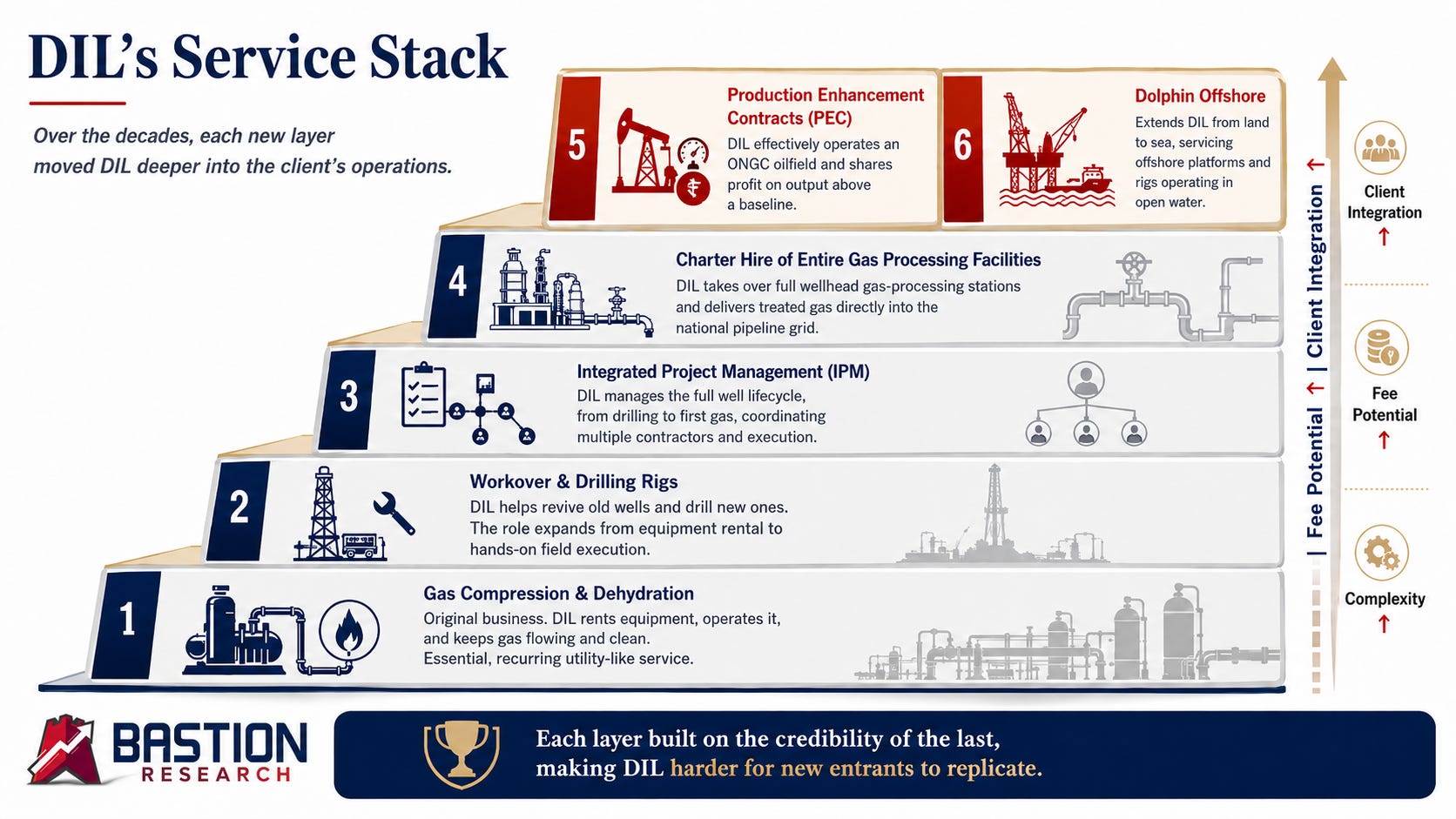

Over the decades, the company has methodically expanded its service portfolio. Think of it as a stack, where each new layer sits on top of the previous one, adds more complexity, commands a higher fee, and brings DIL deeper into its client’s operations.

At the base: gas compression and dehydration, the original business. DIL rents the equipment, runs it, and keeps the gas flowing and clean. Think of it as the utility-meter end of the oil and gas world: unglamorous, essential, and recurring. Above that came workover and drilling rigs: now DIL is not just processing the gas that comes out, it is helping revive old wells that have stopped producing and drilling entirely new ones. The client is now handing over more of the physical work, not just the equipment. Then came Integrated Project Management (IPM): DIL takes responsibility for the entire lifecycle of a well, from the first drill bit to the moment gas starts flowing, coordinating all the specialist contractors and taking the blame if anything goes wrong. After that, the charter hire of entire gas processing facilities: instead of renting individual machines, DIL now takes over an entire gas-processing station at the wellhead, treating and delivering finished gas directly into the national pipeline grid. The client does not need to even look at the site. And now, at the very top of this stack, sit two genuinely new categories: the Production Enhancement Contracts (PEC), where DIL effectively becomes the operator of an ONGC oilfield and shares in the profits of everything it produces above a baseline, and Dolphin Offshore, which takes DIL from land into the sea, servicing the offshore platforms and rigs that operate in open water. Each layer built on the credibility of the last, each one harder for a new entrant to replicate.

The Shift That Changed the Growth Trajectory: Charter Hire of Entire Gas Processing Facilities

Until FY23, DIL provided compression and dehydration as separate services. A client would call them for a compressor today, and perhaps for a dehydration unit next month. DIL would earn from each piece of equipment individually. It was a good business, but a fragmented one.

Since FY23, something structurally changed. DIL began bundling compression, dehydration, separation, and filtration into a single integrated contract: the charter hire of an entire gas processing facility. Under this model, DIL takes raw gas straight from the wellhead, processes it entirely, and injects finished, pipeline-ready gas directly into the GAIL national grid. The client does not touch the equipment, hire the engineers, or worry about uptime. That is entirely DIL’s responsibility. In return, DIL earns a higher blended day rate for a longer contract duration.

Project Jaya, a turnkey Integrated Gas Processing and Compression project for ONGC, is a flagship example of this model. DIL is running similar contracts with Cairn Oil & Gas and ONGC. This structural shift is what has driven the jump in capital employed turnover and the improvement in ROCE over FY23 to FY26.

From Renting Equipment to Running Oilfields: The Next Chapter

The charter hire of integrated gas processing facilities was DIL's first significant move up the value chain. The Production Enhancement Contract (PEC) is its boldest step yet, one that repositions the company from an oilfield services contractor to an upstream field operator.

The Production Enhancement Contract (PEC): A First for DIL

India imports ~85% of its crude oil, a figure that represents a chronic vulnerability in the current geopolitical environment. The government’s strategic imperative is to squeeze more production out of existing, ageing domestic fields, not just find new ones. ONGC manages hundreds of mature fields that have been producing for decades. Many of these fields require focused operational attention, technology upgrades, and new infill drilling to arrest the natural production decline. But ONGC, stretched thin by the demands of massive offshore projects, simply cannot give every mature field the attention it needs.

Enter the PEC model. The best way to understand it is to think of a sales employee at a company. His compensation has two parts: a fixed base pay that he collects every month regardless of how he performs, just enough to cover his living costs, and a variable component, the real money, which is entirely determined by how much he sells above his target. If he smashes his target, he earns multiples of his base pay. If he just meets it, he collects the base and not much more. His entire financial upside is tied to performance.

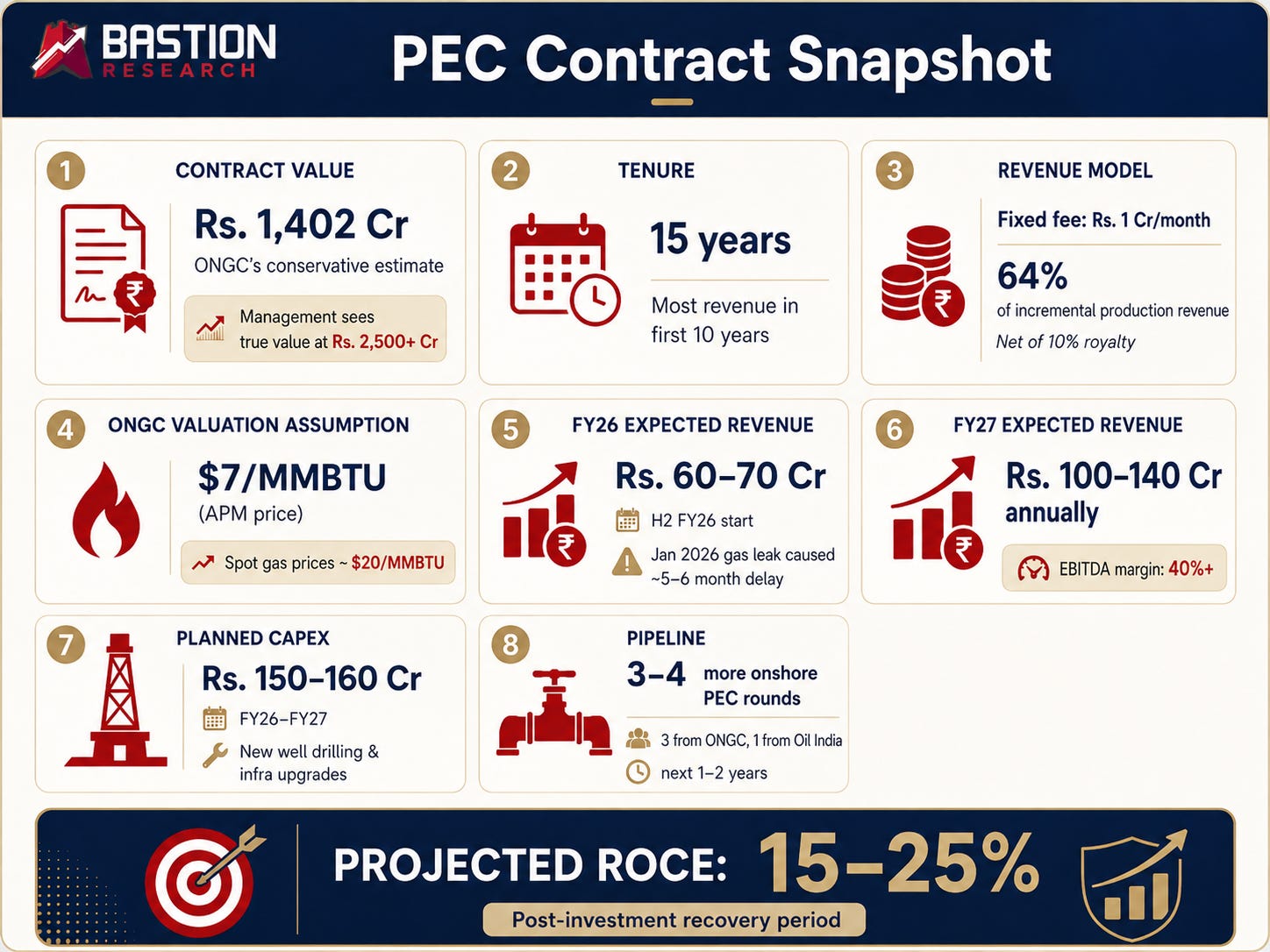

The PEC works exactly like this. DIL collects a fixed base fee of roughly Rs. 1 Crore per month from ONGC, which management openly acknowledges is just enough to cover operating costs. That is the fixed salary. The real money comes from incremental production: every additional unit of gas that DIL extracts above a pre-agreed baseline threshold is split, with ONGC taking 36% and DIL keeping 64% (net of a 10% royalty to the state government). ONGC sets the baseline on the day it hands the field over, factoring in the natural decline of the well over time. If DIL drills new wells, applies better technology, and genuinely revives the field, it earns the lion’s share of the upside. If it simply maintains the status quo, it earns its base fee and little else. The entire incentive structure is skewed towards the upside, exactly like a salesperson working on commission. DIL invests its own capital upfront, bets that it can grow production, and then earns a share of every incremental molecule of gas it extracts over 15 years.

In September 2024, DIL secured its first PEC from ONGC: a 15-year contract for the Rajahmundry Asset in Andhra Pradesh, valued at Rs. 1,402 Crore by ONGC’s conservative estimates. Management believes the true value of the contract, at realistic gas prices and production levels, exceeds Rs. 2,500 Crore. Operations began in Q1 FY26.

The PEC represents a fundamental change in the nature of DIL's earnings. Unlike a charter-hire contract where revenue is fixed and predictable but capped, the PEC has an asymmetric payoff: the better DIL performs at the field, the more it earns. And because ONGC plans to extend PECs to over 100 mature assets, DIL's experience at Rajahmundry is an extraordinarily valuable credential for bidding future rounds.

Buying Broken Assets for Rs. 27 Crore, and Making Them Work

The second major pillar of DIL's transformation is its entry into offshore oil & gas services through the acquisition of Dolphin Offshore Enterprises (India) Limited. This is where management's capital allocation skill becomes most visible.

Dolphin Offshore was founded in 1979. For decades, it was one of India's most respected offshore engineering contractors, serving ONGC, Reliance, Cairn, and L&T Hydrocarbon in diving, subsea inspection, marine logistics, and EPC contracting. Then, in FY20, poor financial management caught up with it. The company became non-operational, accumulated debt, and entered insolvency proceedings under the IBC. Its assets, including a DP2 accommodation barge called Vikrant Dolphin, sat idle for over three years.

It is worth pausing here to note what DIL was at this point in time: a company with a decade of deep onshore experience, a dominant position in gas compression, a growing rig fleet, and zero presence in the offshore world. Everything it knew, every asset it owned, every contract it had executed, sat on land. The offshore oil and gas market is a different beast entirely: it operates in open water, requires different equipment, different certifications, different client relationships, and carries its own set of technical and safety risks. Getting into offshore from a standing start typically takes years of credentialing.

DIL identified the strategic shortcut: here was a company with valuable offshore credentials, established client relationships, and idle but refurbishable assets, all available at a fraction of replacement cost through the IBC resolution process.

In January 2023, DIL acquired a 75% stake in Dolphin Offshore through its wholly-owned subsidiary for a total consideration of just Rs. 27 Crore. To put this in perspective: building a comparable offshore services business from scratch, securing vessel assets and client credentials without the IBC shortcut, would have taken 2 to 3 years and hundreds of crores. DIL bypassed all of that with a single cheque.

Then came the transformation. DIL invested ~Rs. 170 Crore in refurbishing the Vikrant Dolphin, now renamed Prabha. Think of the Prabha as a floating hotel for offshore oil rig workers. When an oil company is drilling or doing maintenance work on a platform out at sea, hundreds of engineers and crew members need somewhere to live, sleep, eat, and rest between their shifts. They cannot commute from shore every day. The Prabha is that home away from home: a large, purpose-built accommodation vessel that moors alongside an offshore platform and houses the entire crew for months at a time, complete with cabins, dining facilities, recreation rooms, a medical bay, and communications equipment on board. The client pays a fixed daily rate simply for the privilege of having this floating hotel parked next to their platform.

What makes the Prabha especially valuable is its DP2 (Dynamic Positioning Class 2) designation. DP2 means the vessel can hold its position precisely in open water without anchors, using its own thrusters and GPS-based positioning systems. This is critical when working alongside sensitive offshore infrastructure where an uncontrolled drift could cause catastrophic damage. There are only 6 to 7 such DP2-classified accommodation barges worldwide. The Prabha was commissioned in Mexico in Q1 FY26 and leased on a three-year charter worth ~USD 33 Million (~Rs. 280 Crore), generating Rs. 90 to 100 Crore in annual revenue at 60 to 65% EBITDA margins.

The math here is compelling. Total investment (acquisition + refurbishment) = Rs. 197 Crore. Annual EBITDA from Prabha alone = ~Rs. 60 Crore. That is a roughly 30% EBITDA return on a single asset. Management has been clear that Dolphin will continue to add offshore assets over time, but only against firm, confirmed client orders. No asset acquisition will precede a contract. Beyond that, specifics on what comes next and when remain to be communicated.

To put the value created here in stark perspective: Dolphin Offshore is a listed entity on Indian exchanges, and as of writing, carries a market capitalisation of approximately Rs. 1,600 Crore. DIL holds a 75% stake in it. That means DIL’s stake in Dolphin alone is worth roughly Rs. 1,200 Crore on the market today, built on a total investment of just Rs. 197 Crore. The Rs. 27 Crore acquisition cheque and the Rs. 170 Crore refurbishment spend have, at current market prices, generated over six times the invested capital in market value. Whatever your view on the broader Deep Industries thesis, this single transaction is a case study in astute capital allocation.

Kandla Energy & Chemicals: Backward Integration

In March 2025, DIL acquired 100% of Kandla Energy and Chemicals Limited for Rs. 2 Crore. Another distressed asset. Kandla’s manufacturing facility produces a specific chemical that DIL consumes heavily in its drilling operations. By bringing this in-house, management calculates an improvement in operating margins of 1.5 to 2%. Additionally, Kandla came with accumulated inventory losses that can be written off for tax savings.

Two acquisitions. Both distressed. Both acquired at fractions of fair value. Both serving clear strategic purposes. This “acquire-clean-revive” playbook is a distinct competitive capability, one that requires the kind of hands-on operational skill that cannot easily be replicated.

By acquiring old assets from the secondary market and deploying them in high-rate environments, management is executing a high-ROCE strategy that most Indian mid-caps simply don’t have the technical competence to attempt.

The Numbers Tell a Story, If You Know How to Read Them

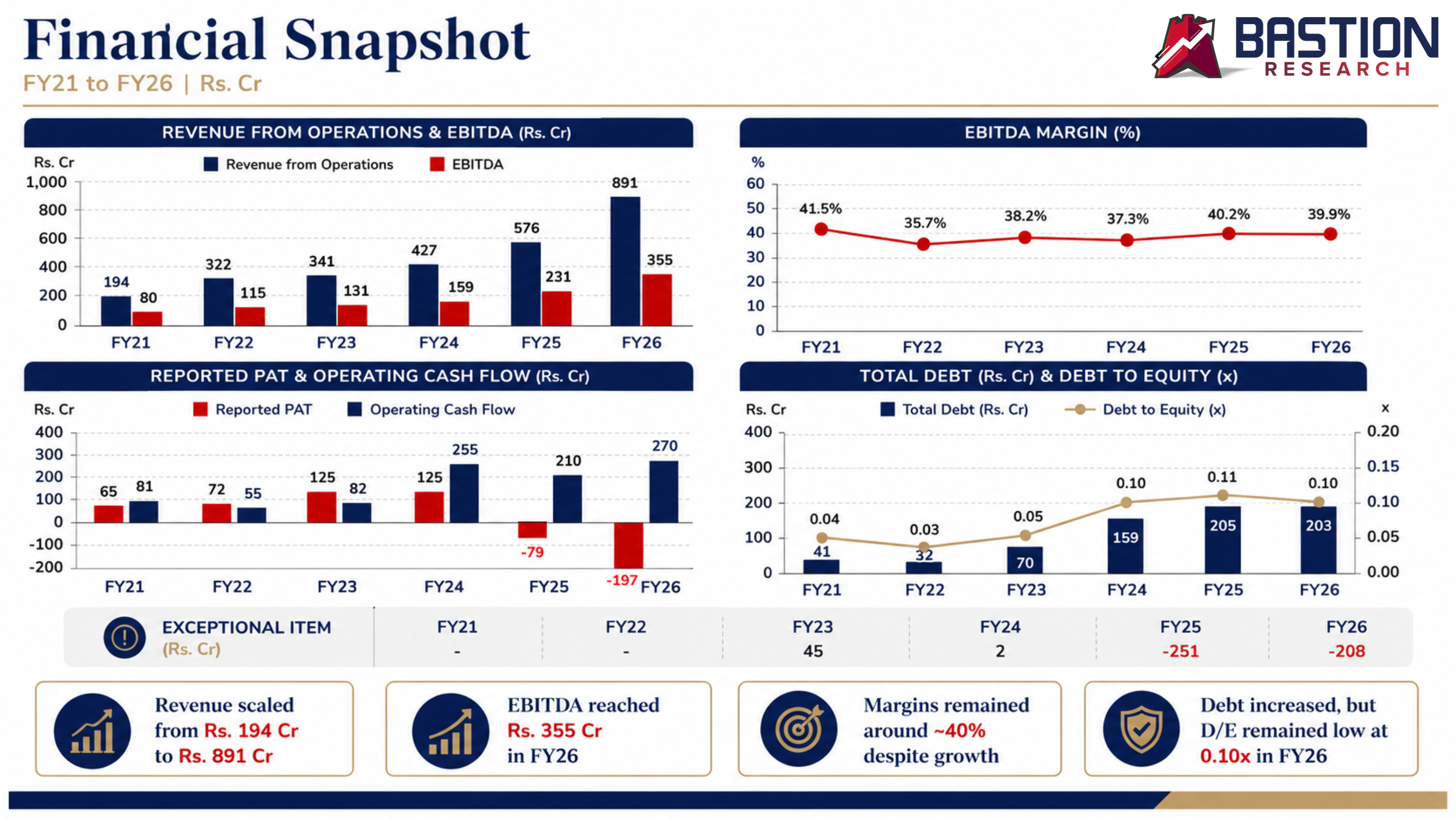

Let us now look at the financials. Across the board, the operational and underlying financial story is one of structural improvement. The confusion arises, as we will discuss in the next section, from the way exceptional items have clouded the reported profit numbers.

The headline story from FY26 results is exceptional: revenue grew 55% YoY to Rs. 891 Crore, EBITDA grew 47% YoY and Operating cash flows grew 29% YoY to Rs. 270 Crore. The balance sheet remains pristine: Debt-to-Equity at 0.10x, with the company generating positive operating cash flows for five consecutive years.

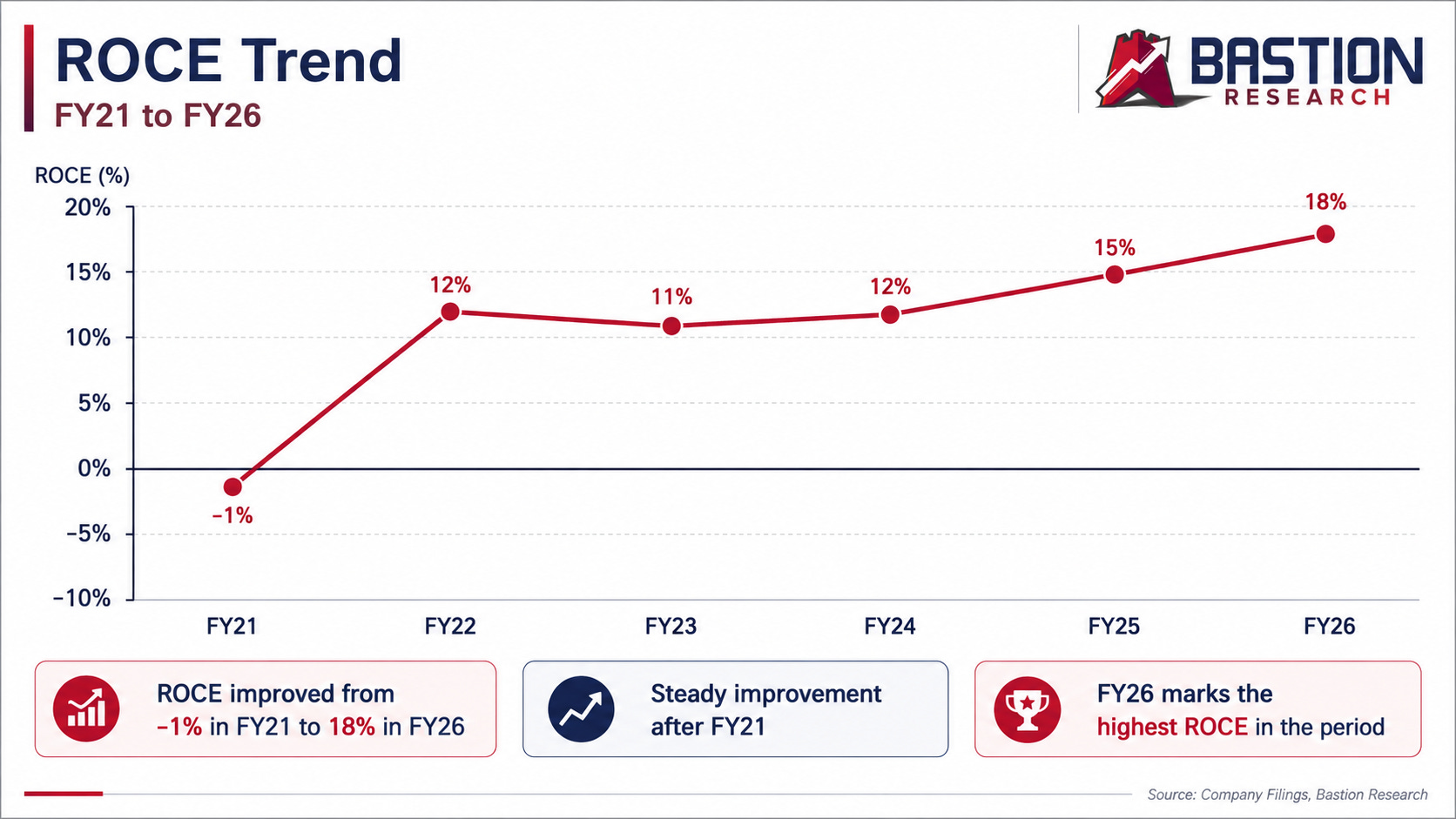

The ROCE Story: The Most Important Metric to look at

Return on Capital Employed (ROCE) is the most honest measure of business quality for a capital-intensive company like DIL. And the ROCE trajectory is precisely what the bull case rests on.

India’s Energy Ambition: The Wind Beneath DIL’s Wings

DIL does not operate in a vacuum. Its growth is anchored to a powerful macro tailwind: India’s aggressive push to reduce its dependence on imported hydrocarbons.

India imports ~85% of its crude oil needs, a figure that represents a chronic vulnerability in the current geopolitical environment. The government’s response has been a sustained, multi-year push to boost domestic oil and gas production. ONGC and Oil India have announced significant capital expenditure programs for exploration and production in 2025 and 2026. The OALP (Open Acreage Licensing Policy) is bringing new exploration blocks to market. And most critically for DIL, the PEC framework is being aggressively expanded, with ONGC targeting 100+ mature field contracts over the coming years.

This is not cyclical spending. This is strategic, policy-driven, long-duration capex, the best kind for a company with long-term, fixed-rate contracts like DIL. Even in a world where crude oil/natrual gas prices correct significantly, the government’s energy security imperative means PSU’s exploration and production spending is unlikely to be dramatically curtailed. DIL’s contracts, once awarded, are typically 3 to 15 years in duration. A 20% decline in crude/NG prices does not cancel a workover rig contract that was signed at a fixed day rate 6 months ago.

So Why Is It Trading at 8x PE? Here Is What We Think.

We want to be upfront about something. Nobody rings a bell to explain why a stock is priced where it is. The reasons below are our best attempt at reading the market's mind, not a definitive list. The truth is probably a combination of all of them, weighted differently by different investors. With that caveat, here is what we think is keeping the valuation down.

1. The Sector Gets Low Multiples, Regardless of the Company

The oil and gas services industry is structurally valued at low PE multiples across the world. It is a capital-intensive, cyclically exposed, PSU-dependent business where most investors assume growth will eventually fade as India transitions to cleaner energy. The market applies a sector-level discount first, and then asks questions. Deep Industries, despite its superior margins and growing ROCE, has not yet managed to separate itself from this sector-wide perception. Investors looking for "compounders" in high-multiple sectors are simply not looking at oilfield services at all, and that structural indifference keeps a lid on valuation regardless of individual company merit.

2. Customer Concentration: One Bad Day with ONGC Wipes Out Most of the Revenue

In FY25, ONGC contributed roughly 54% of DIL's total revenue. Even as this has improved to below 40% in FY26, the dependence remains uncomfortably concentrated. And it is not a theoretical risk: DIL has had real disputes with ONGC in the past, including arbitration proceedings over gas compression contracts. The relationship between a PSU and a private contractor in India can be subject to delays, renegotiations, and bureaucratic friction. Any meaningful deterioration in that relationship, or a significant cut in ONGC's capex budget, would hit DIL's revenues hard and fast. The market prices this risk in by keeping the multiple suppressed.

3. Related Party Transactions: Capital Being Deployed Outside the Business

Prabha Energy, a sister concern of DIL owned by the same promoter group, has received an unsecured loan of Rs. 90.6 Crore from DIL at 12% interest. Management expects full repayment in near term. But similar transactions may occur in the future, suggesting this is a feature of the promoter group's capital allocation approach, not a one-off anomaly. For minority investors, there is always an uncomfortable question when a company lends its own capital to a promoter group entity at a fixed rate, particularly when that capital could be deployed into high-ROCE businesses within DIL itself. It is not a smoking gun, but it is a needle that keeps investors cautious.

4. Historical Governance: The Past Leaves a Shadow

DIL's history includes a CBI inquiry against the company (since resolved) and an insider trading charge against the MD in 2015. These are historical incidents, and no current accounting discrepancies have been identified. But markets have long memories. Investors who ran these names through their governance filters in the past may have marked it a "no" and never revisited. Governance concerns, once embedded in investor’s memory, are slow to reverse even when the present-day reality has changed.

5. The Charter Hire Business Is Fundamentally an Equipment-Leasing Business

This is perhaps the most intellectually honest reason of all. Strip away the PEC and the offshore story, and what you have is a company that buys expensive equipment and rents it out at a margin. Charter hire, at its core, is equipment leasing: it generates good margins and stable cash flows, but it does not inherently produce the kind of asset-light, high-ROCE returns that the market rewards with premium multiples. The ROCE of the core legacy business, before you adjust for goodwill and before the new businesses kick in, has historically hovered in the 9 to 12% range. It is the PEC and offshore segments that could push ROCE meaningfully higher, but those are still unproven at scale. The market may simply be refusing to pay up for something it cannot yet see in the numbers.

6. Two Years of Reported Losses: The Accounting Noise Problem

In FY25, DIL reported a loss of Rs. 79 Crore. In FY26, despite a blowout operational year, reported PAT came in at Rs. 197 Crore, far below what the underlying performance would have suggested. The culprit in both years: exceptional write-offs of legacy receivables inherited from the Dolphin Offshore and Kandla Energy acquisitions. These write-offs are non-cash, non-recurring, and disclosed as exceptional items. They do not affect operating cash flows. But for any investor running a screen or a quick glance, a company that reported a loss in FY25 and a confused FY26 is not one that invites further investigation.

Kandla's legacy receivables have been fully written off, and that chapter is closed. Dolphin's position is more nuanced: management still expects to recover a portion of its legacy receivables and has not written them off entirely. That means the possibility of further exceptional charges in FY27, if recovery efforts disappoint, cannot be fully ruled out. The accounting noise may be largely behind us, but calling it completely done would be premature.

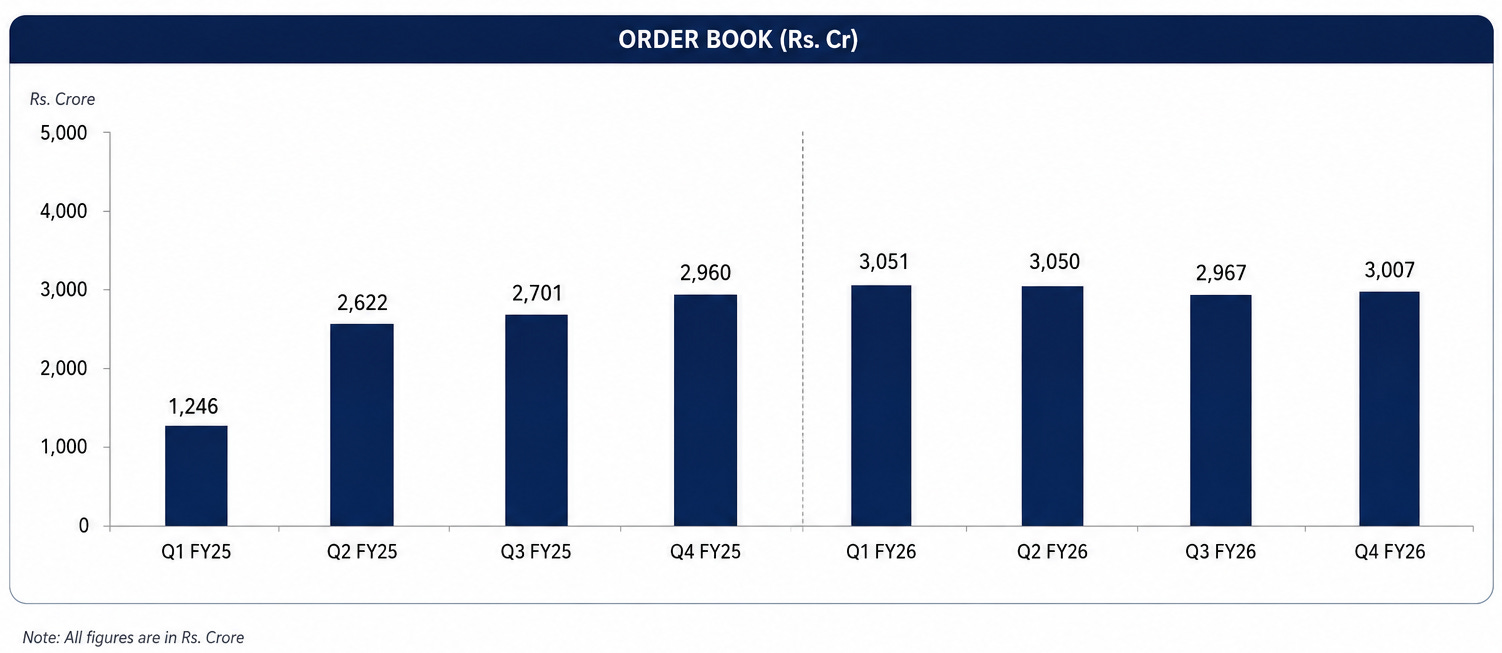

7. The Order Book Has Gone Nowhere for Five Quarters

DIL's order book has hovered around Rs. 3,000 Crore for the last four to five quarters, barely moving despite the company executing at a rapid pace. If revenues are growing at 55% but the order book is not expanding, a fair question is: where does the next leg of growth come from once the current backlog runs out? The answer lies in new PEC rounds and confirmed Dolphin vessel contracts, both real opportunities, but neither yet in the order book. Until they are, the market may not want to pay for growth it cannot see. A new PEC win or a confirmed vessel contract may well be the most important near-term catalyst for a re-rating.

8. PEC Execution risk

The gas leak at Well Mori #5 in January 2026 caused a 5 to 6 month delay in the PEC production ramp. More broadly, the PEC is a fundamentally different business from charter hire: the revenue depends entirely on DIL's ability to physically increase reservoir output, which is subject to geological uncertainty, regulatory friction, and execution risk in a way that renting equipment simply is not. The market may be justified in applying a discount until DIL proves, over multiple quarters, that it can consistently extract and grow production from the Rajahmundry asset.

Deep Value or Value Trap? The Story Is Still Being Written.

We have spent several thousand words trying to answer the question in the headline. And we will be honest with you: we do not have a clean answer. The story is genuinely still unfolding, and there are more questions than there are certainties.

The numbers are hard to argue with. Revenue at Rs. 891 Crore in FY26 is a 55% YoY jump. Operating cash flows are at an all-time high of Rs. 270 Crore. The balance sheet is nearly debt-free (D/E: 0.10x). ROCE has improved to ~18%. The order book at Rs. 3,050 Crore provides revenue visibility for next 12-18 months. Receivables have cleaned up dramatically. The stock trades at ~8x FY26 earnings, in line with comparable oil and gas services companies trade between 10-20x PE. On the numbers alone, this does not look like a business that deserves to trade this cheap.

And yet, the market is saying something. It almost always is. The question is whether the market is right, or whether it is simply confused by accounting noise and sector-level indifference. That is the central question we cannot definitively answer. But here are the questions we are sitting with:

Five Things We Are Still Thinking About

Does this sector ever get a high valuation, regardless of growth? Oil and gas services companies globally trade at compressed multiples. The energy transition narrative hangs over the entire sector. Is Deep Industries permanently condemned to a low PE simply because of the industry it operates in, no matter how well it executes? If the answer is yes, then the 30% growth story may be real but then investor returns will mirror business performance and limited scope for re-rating.

The market has watched this company grow at 30%+ for five years and still hasn’t re-rated it. Can five years of consistent delivery really be dismissed as a one-off? If the market were simply waiting for more proof, it has had plenty. The CAGR is real, the operating cash flows are positive, the order book is large. Something else must be holding the multiple back, and it may be structural rather than temporary.

Is there something in the accounting that our framework missed? We ran the numbers through our Accept-Reject framework. The CFO-to-EBITDA ratio is healthy. Operating cash flows are consistently positive. Receivables have cleaned up. Goodwill is stable. We did not find anything material.

Is the PEC a genuine earnings transformer, or a high-stakes bet that could disappoint? The gas leak at Rajahmundry was a real reminder that this is not like renting a compressor. Operating an oilfield is a different kind of business: messier, less predictable, and dependent on what is underground rather than what is in a contract. The next 4 to 6 quarters of PEC execution will answer this question far better than any analysis can.

Will the related party transactions stay manageable, or become a pattern that minority investors cannot tolerate? Management may do it again in the future. The interest rate is accretive. The amounts are currently not large relative to the company’s size. But the precedent is set, and it is something to watch closely.

Here is where we land, for now. The growth is real. The balance sheet is clean. The competitive position is defensible. The macro tailwind is genuine. The valuation is compelling on almost any metric you apply. And yet the story has enough open threads, on governance, on sector re-rating potential, on PEC execution, on the accounting clean-up, that we cannot say with complete confidence that the market is simply wrong.

What we can say is that we will be watching this company extremely closely over the next several quarters. The FY27 results, the first ones free of any exceptional noise, will be critical. The PEC production ramp at Rajahmundry will be critical. Any new PEC contracts from ONGC or Oil India will be critical. The related party transactions with Prabha Energy will need to stay at current levels or reverse. And the Dolphin fleet expansion, if it happens only against firm orders and at the right capital cost, could be a genuine earnings step-up.

Whether or not we invest is a question we are still working through. But if you want to know when we reach that conclusion, and whether we decide to add it to our Bastion Core portfolio, there is only one way to find out.

Become a Bastion Core subscriber. That is where the live portfolio decisions, the quarterly tracking, and the conviction updates will live. This newsletter is the research. What happens next is the story.

IMPORTANT NOTE

We run a Smallcase called Asymmetric Growth — a curated portfolio built around one idea: find businesses where the upside is large and the downside is limited.

No noise. And yes, we use a bit of momentum where it works in our favour — but only to boost returns, never to chase them.

Just disciplined, research-backed investing.

If that sounds like your kind of portfolio, this is where you want to be.

If you know someone who’s tired of guessing and ready to invest with conviction, send this their way.

Explore our Newsletter Archive to catch up on previous editions.

😂Meme of the Week😂

🤝Connect with us

We’d also love to hear your thoughts and feedback on various platforms where we are active. Connect with us below:

Know more about Bastion Research @ Website,

Get daily updates from Bastion Research @ Twitter (X), @ WhatsApp Channel, @ LinkedIn and, @ Stocktwits

Watch insightful videos and company deep dive podcasts “Made in India” by Bastion Research @ YouTube

If you enjoyed reading this newsletter, please feel free to share it with others who might find it insightful.

Happy Investing!!!

Disclaimer: These insights are based on our observations and interpretations, which might not be complete or accurate. Bastion Research and its members may or may not have stakes in companies mentioned. This newsletter is for educational purposes only and is not intended to provide any kind of investment advice. Please conduct your own research and consult your financial advisor before making any investment decisions based on the information shared in this newsletter.

👍👍👍👍👍👍

❣️❣️❣️❣️❣️❣️

🙏🙏🙏🙏🙏🙏