The TIRUPATI Files

A cooking oil brand. A ₹5,600 crore financial scandal. A family navigating the shadow of its own past. And a ₹5.37 crore acquisition that may put a ₹5,000 crore business onto Dalal Street.

The oil in your kitchen may have a complicated history

There is a good chance that somewhere in your home, or in your parent's home, or in a restaurant where you last ate, there is a pouch or a tin of Tirupati cooking oil. The brand has that kind of reach. In Gujarat and the surrounding markets, Tirupati has a commanding presence in the cottonseed segment, with an ~40% market share at its peak. It sits alongside the national giants, quiet and familiar, the kind of brand that does not need to advertise loudly because it has been on the shelf for three decades.

It covers cottonseed oil, rice bran oil, sunflower oil, and a growing range of consumer food products including packaged namkeens. It is a real brand with real consumer equity, built over more than twenty years of consistent distribution.

There is a reasonable chance that this brand, one you recognize, one you may have trusted is on its way to a stock exchange listing. Not through the conventional IPO route, where a company files a prospectus, invites public scrutiny, discloses every material litigation, and faces institutional due diligence. But through a back door: a ₹5.37 crore acquisition of a near-dormant listed NBFC shell that may be the most carefully engineered route to Dalal Street you will encounter in recent memory.

To understand why the back door was chosen over the IPO route, you need to understand this group's history. And that history is anything but simple.

Behind that familiar brand sits one of India’s most complicated corporate stories. A story that involves two brothers, a commodity exchange that collapsed in the biggest financial scandal in India’s spot market history, a founding promoter whose chapter ended under a cloud of criminal proceedings, and a next generation now steering the ship toward a listing that the group could never have achieved the conventional way.

This is The Tirupati File.

TWO High-Conviction Stock Ideas - Free Access

We want to give you access to TWO of our detailed research notes from Bastion CORE, completely free of charge.

Why are we doing this?

Because we believe the quality of our work is our best marketing. We want you to see exactly how deep we go.

At Bastion CORE, we don’t just give you a ticker. We break down the business model, the valuation logic, and the risk factors. We do months of work so you don’t have to.

Get the Research Notes: Click the link below. We will immediately email you the two research reports, along with details on how Bastion CORE can help you build a stronger portfolio.

Back to the story…

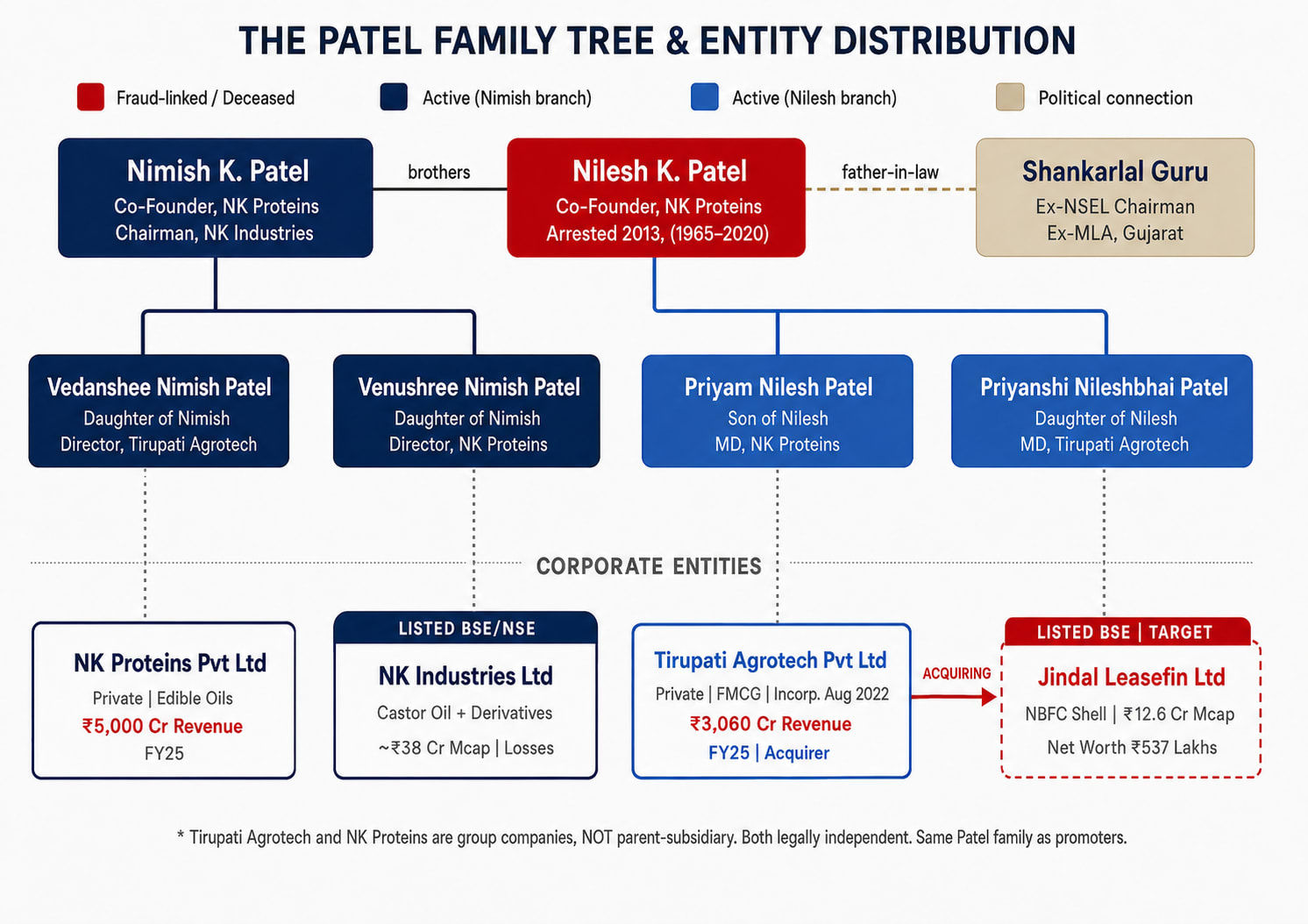

The Patel family, mapped

The story begins with two brothers from Gujarat's Mehsana district. Nimish Patel and Nilesh Patel incorporated what was then called Maruti Proteins Limited in March 1992. The name changed to NK Proteins Private Limited in February 1993. Over the next two decades, they built one of India's largest edible oil processing operations.

They were not equal partners in public perception. Nilesh was the face. He was the trader, the politically connected one, the man who understood commodity markets in ways that made bankers and exchange operators pay attention. Nimish was the industrialist, the one running manufacturing. They divided the empire along those lines.

Here is the family structure as it stands today, which is critical to understanding every corporate move that follows.

What you see in that diagram is the key to everything else. The Patel family does not run a single clean corporate structure. They run a web of entities where each entity has a specific function, a specific history, and now, it appears, a specific role in a larger plan.

How a spot exchange became a ₹5,600 crore black hole

To understand why NK Proteins cannot do a conventional IPO, you need to understand the NSEL crisis. And to understand the NSEL crisis, you need to understand how a commodity exchange is supposed to work.

The theory: clean, simple, transparent

A spot exchange is the digital equivalent of a physical mandi. A farmer, a processor, or a trader wants to sell a commodity today. A buyer wants to buy it today. They meet on an exchange platform, agree on a price, and the transaction settles within two days. Money changes hands. Physical goods change hands. Done. This is essentially how we buy or sell stocks today on NSE or BSE.

The National Spot Exchange Limited (NSEL) was launched in 2008, promoted by Jignesh Shah’s Financial Technologies India Limited, with NAFED as co-promoter. It was conceptualized in 2004 with exactly this mandate: create India’s first electronic spot exchange for agricultural commodities. Simple, efficient, price-transparent.

The reality: a disguised lending machine

To understand what NSEL was really doing, forget commodities for a moment. Think about the stock market, which most investors understand better.

Suppose you log into your broker and buy shares of Reliance on NSE today. You pay money, the shares come into your demat account, and from that point onwards, your return depends on the market price. If Reliance rises, you make money. If it falls, you lose money. There is no guaranteed return.

Now imagine a strange version of the stock market.

A broker tells you:

“Buy Reliance today for Rs 1,000. At the same time, we will arrange for someone to buy it back from you after 35 days at Rs 1,015. You do not have to worry about price movement. Your return is locked in.”

To a normal investor, this sounds like magic. You are not taking market risk. You are not studying the Company. You are not betting on demand, supply, valuation, or earnings. You are simply putting in Rs 1,000 today and getting Rs 1,015 after 35 days.

That is not investing. That is lending.

The share is only being used as a wrapper to make the transaction look like a market trade. In economic substance, the person taking your Rs 1,000 is borrowing money from you for 35 days and promising to repay it with interest.

NSEL’s paired contracts worked in a similar way.

An investor would buy a commodity today at one price and simultaneously enter into another contract to sell the same commodity after 25 to 35 days at a higher price. The difference between the two prices became the investor’s fixed return. Brokers marketed this as arbitrage, almost like a risk-free product earning 14-15% annualised returns.

But the investor was not really betting on the price of castor seed, sugar, paddy, or any other commodity. The investor was effectively lending money to a borrower, while the commodity contract created the appearance of a legitimate exchange transaction.

The problem was that this entire structure depended on one crucial assumption: the commodity actually existed in the warehouse.

If the borrower failed to repay, investors were supposed to be protected by the goods lying in NSEL-approved warehouses. In theory, the stock could be sold and investors could recover their money.

But when the crisis broke, that assumption collapsed. In several cases, the warehouse stock was missing, inflated, or simply did not match the paper claims. The “collateral” backing thousands of crores of investor money was not really there.

So what looked like a safe exchange-backed arbitrage product was, in reality, an unsecured lending machine wearing the clothes of a commodity trade. And once the Forward Markets Commission stopped NSEL from launching fresh contracts on July 31, 2013, the rollover chain broke. Borrowers could no longer raise fresh money to repay old investors. The structure collapsed, leaving ~13,000 investors stuck in a ~Rs 5,600 Cr settlement crisis.

In simple words, NSEL was not matching genuine commodity buyers and sellers. It was matching investors hungry for fixed returns with borrowers hungry for short-term funding. The commodity was the costume. The loan was the real business.

NK Proteins: the single biggest borrower in the wreckage

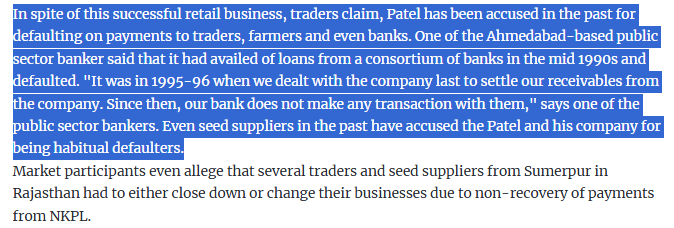

Among the 24 borrowers who caused the ₹5,600 crore collapse, one of them was responsible for nearly one-sixth of the entire default, almost Rs. 970 Cr on its own. Its name: NK Proteins Private Limited. (aka Tirupati Brand we all know).

Let those numbers sink in. NK Proteins owed nearly 9 times its entire net worth to NSEL investors. By October 2013, it had repaid just ₹7.10 crore of the ₹970 Cr it owed. The default-to-net worth ratio of ~9x makes it not just the largest defaulter, but one of the most egregious cases of overleveraging the crisis produced.

Further, this is not the first time NK Proteins payment discipline had come under question. Read this statement 👇

The fake godowns

NK Proteins had been using the NSEL platform in exactly the way we described: raising money from investors using commodity contracts backed by supposed warehouse stocks. Nilesh Patel himself is credited in the NSEL CEO’s court affidavit with having conceived the T+3 and T+36 contracts in castor seed, the specific paired contract structure that created the framework for this level of borrowing.

In a physical warehouse in Gujarat, NK Proteins claimed to hold castor seeds. The warehouse receipts served as the collateral backing NSEL investors’ positions. When investigators arrived to verify those stocks, they found no actual inventory. It is possible the stock had been sold to generate cash. It is possible it was never there in the first place. Either way, the receipts were false or wildly inflated. NK Proteins had borrowed nearly ₹970 crore on the strength of collateral that did not exist.

What makes this chronology particularly damning is when the exchange management actually knew. The former NSEL CEO, Anjani Sinha, provided this in his affidavit before the court:

“By end of December 2011, it was known to us that he was not having stock to back the exposure. Still, we allowed him to continue because of the fear of widespread default if we chose not to allow him to roll over.”

Anjani Sinha, Former CEO, NSEL — in his affidavit before the court

Read that carefully. By December 2011, NSEL's own management already knew NK Proteins had no stock to back its exposure. They did not halt the positions. They did not alert investors. They rolled everything forward for another 18 months until the FMC's July 2013 intervention made rolling impossible and the collapse became unavoidable. Nilesh Patel was not caught by a surprise audit. The exchange that should have been protecting investors chose, for 18 months, to look away.

Where the money went

Investigations by the Economic Offenses Wing (EOW) of Mumbai Police revealed that NK Proteins did not keep the money it raised from NSEL investors on its own books. ~₹350 crore was used to fund a 50:50 joint venture with the Adani Group’s agro trading arm, forming a company called AWN Agro Private Limited, which briefly became India’s largest castor oil exporting entity.

The rest was not sitting in NK Proteins either. The EOW found that funds had been diverted to Tirupati Retail Private Limited, a group entity promoted by Darshan Baldevbhai Patel, a cousin of Nimish Patel. The money raised from 13,000 investors had been dispersed across the group before the crisis broke.

The Adani JV Angle

AWN Agro Private Limited, the 50:50 castor oil export JV between NK Proteins and what was then Adani Wilmar’s agro trading business, had already collapsed by early 2013, reportedly called off after a two-year association. Nilesh Patel had assured NSEL that this JV’s cash flows would help him liquidate ₹200 crore of positions. When the JV fell apart, that exit route closed with it.

The chairman’s son-in-law

If the NSEL story were simply a case of a reckless borrower and a negligent exchange, it would be scandalous enough. But there is a layer that makes it genuinely extraordinary.

Shankarlal Guru was the Chairman of NSEL. He was also a former Member of the Legislative Assembly from Gujarat. And he was Nilesh Patel’s father-in-law.

The chairman of the exchange had his son-in-law as the exchange’s single largest borrower, to the tune of nearly ₹970 crore. The NSEL Investors’ Forum stated publicly: “A chairman cannot be an innocent bystander when a fraud of ₹5,600 crore is being committed and almost 20% has gone to his son-in-law.”

Shankarlal Guru resigned from NSEL’s chairmanship on August 19, 2013, shortly after the crisis broke. Investigators alleged that this family connection allowed NK Proteins to roll its contracts forward far beyond what any genuinely arm’s-length exchange would have permitted. As the NSEL CEO’s affidavit makes clear, the exchange management knew NK Proteins had no stock as early as December 2011 and continued rolling positions for another 18 months regardless — a decision that is difficult to explain without the weight of that family relationship in the background.

The political economy of why that was allowed to happen is not difficult to reconstruct.

The arrests, the asset seizures, and the ICRA downgrade spiral

On October 22, 2013, the Economic Offenses Wing of Mumbai Police arrested Nilesh K. Patel, Managing Director of NK Proteins. He was sent to police custody, later released on bail. He was the first borrower in the NSEL crisis to be arrested.

The consequences cascaded quickly after:

How a company survived the unsurvivable

On paper, NK Proteins should not have survived.

The Company was the largest borrower in the NSEL collapse. Its promoter was arrested. Its ratings were downgraded and then suspended. Bank limits were cancelled. Properties were attached. Offices, factories, land parcels and even the Kadi plant came under enforcement action.

In most businesses, this would be the end of the story.

But NK Proteins was not a normal balance-sheet business. It was sitting on something more difficult to attach than land or machinery: a fast-moving consumer brand.

The government could attach properties. Lenders could pull limits. Rating agencies could walk away. But the Tirupati pouch on the retail shelf did not carry a footnote saying “linked to the NSEL crisis.” For the end consumer, it was still the familiar oil brand they had bought for years.

The more interesting question is not why consumers kept buying. It is how the supply side kept functioning.

The answer appears to lie in three things.

First, attachment did not necessarily mean operational closure. Many attached assets become legally encumbered, but they are not always physically sealed or immediately liquidated. The factory may be under legal restriction, but the business can continue operating in the gaps, especially until courts decide how and when assets should be monetised.

Second, the group had operating flexibility. Public reports from 2014 suggested NK Proteins had owned crushing capacity, leased capacity, and additional manufacturing presence. That means the group was not dependent on one single asset. Even if owned assets were frozen, production could potentially be routed through leased or alternate arrangements.

Third, the Tirupati ecosystem was not housed in one clean corporate box. Public reports from 2013 indicate that Tirupati Retail, described then as the producer and retailer of the Tirupati edible oil brand in Gujarat, was not included in NK Proteins’ reported NSEL exposure and net worth. This matters because it suggests that the brand, distribution, manufacturing and trading functions were spread across group entities rather than sitting neatly inside one balance sheet.

So NK Proteins did not survive because the scandal was small. It survived because the operating business was bigger, messier, more distributed, and more resilient than the legal case against one entity.

The fraud hit the balance sheet.

The brand kept moving through the market.

The result is that NK Proteins today reports ₹5,010 crore in revenue for FY25, with ₹58.6 crore in net profit and ₹113 crore in EBITDA. The business that defaulted on ₹970 crore and repaid ₹7 crore is now a ₹5,000 crore operation with healthy cash generation.

NSEL investors, meanwhile, are still waiting.

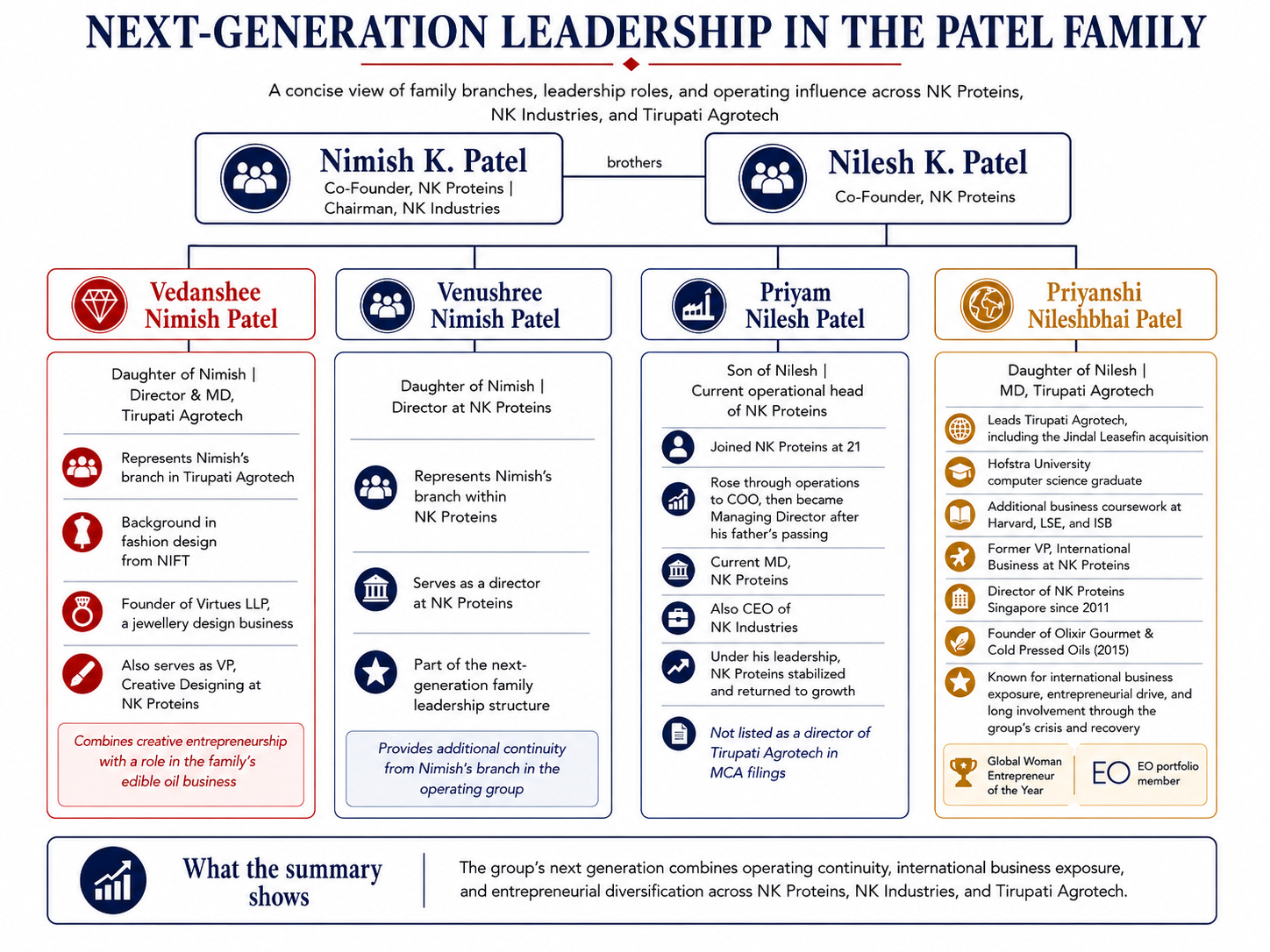

The next generation: same family, new faces

Nilesh Patel passed away in 2020. By then, his children and his brother’s children were already embedded across the group’s entities, having joined the business years before the NSEL crisis even broke. The next generation did not inherit a problem from a distance. They were present.

It is worth introducing each of them, because they are the people who now control the entities at the centre of this story.

Her presence on the Tirupati Agrotech board is notable: both branches of the Patel family, Nilesh's and Nimish's — are formally represented in the entity now executing the Jindal Leasefin acquisition. This is not a transaction driven by one side of the family. The corporate restructuring benefits and is overseen by the entire Patel family, across both branches.

The question of what they knew

The NSEL crisis reached its peak in 2013. Priyam joined NK Proteins around 2010. Priyanshi was VP of International Business at NK Proteins from 2010 to 2011, and Director of the Singapore entity from October 2011 — the exact month, per the NSEL CEO’s court affidavit, by which the exchange management already knew NK Proteins had no stock to back its exposure. Vedanshee has been at NK Proteins since 2016.

The claim that the next generation was unaware of what was happening in the business they were actively working in during the crisis years is difficult to sustain. The corporate restructuring that followed the creation of Tirupati Agrotech, the loading of group revenue into it, the acquisition of Jindal Leasefin, benefits precisely the same family that was present through those years. The NSEL liability to 13,000 investors remains unresolved. The fruit, the evidence suggests, has not fallen far from the tree.

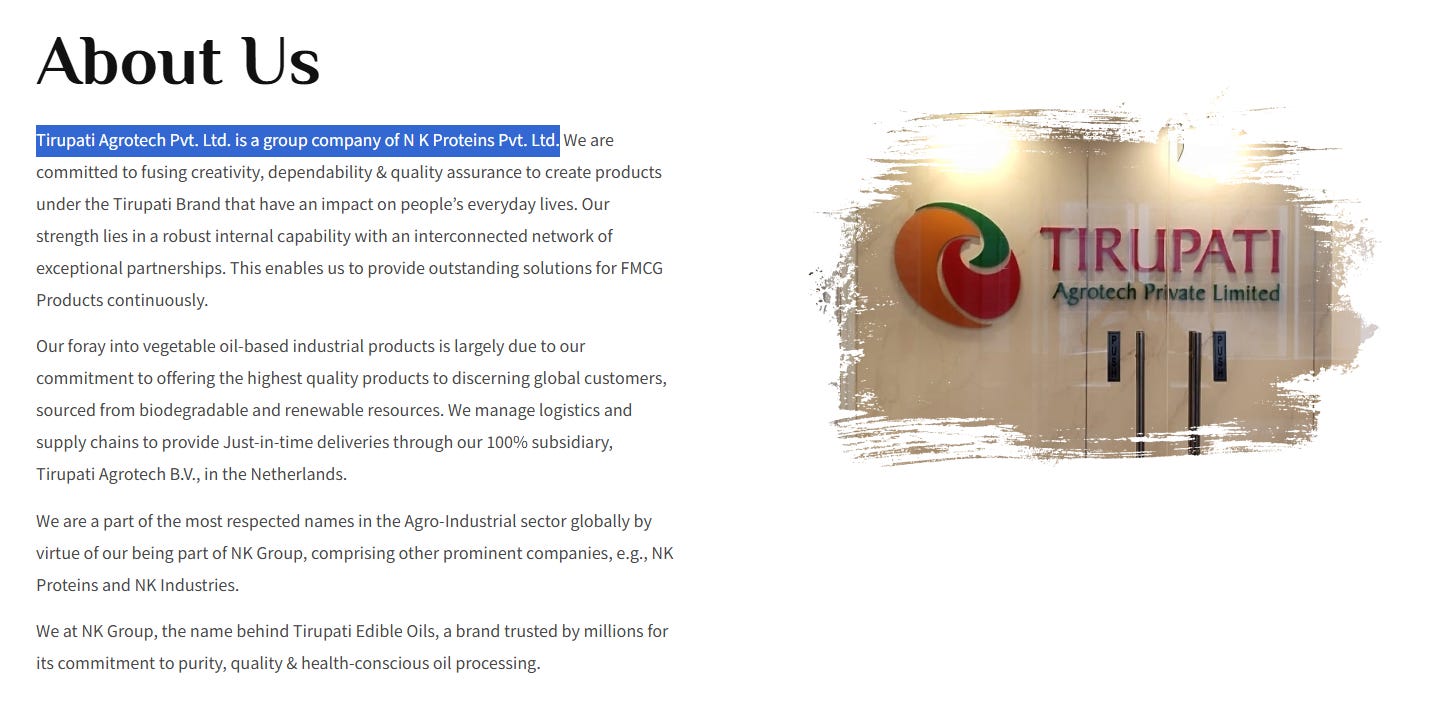

The clean entity: Tirupati Agrotech, born August 2022

On August 20, 2022, a new company was registered with the Registrar of Companies in Ahmedabad. Its name: Tirupati Agrotech Private Limited. Its registered address: 7th Floor, Popular House, Ashram Road, Ahmedabad. Its email domain: nkil@nkproteins.com. Its authorized capital: ₹10 lakh. Its paid-up capital: ₹1 lakh.

Tirupati Agrotech’s own website describes itself as “a group company of N.K. Proteins Pvt. Ltd.” It further states that it “continues to market high-quality products from NK Proteins and NK Industries while developing our range of consumer products.”

In legal terms, Tirupati Agrotech and NK Proteins are not parent and subsidiary. There is no disclosed cross-shareholding or holding company structure between them in any public filing. They are group companies under a common promoter family, legally independent siblings.

This distinction matters more than it might initially appear. We will return to it in the reverse merger section.

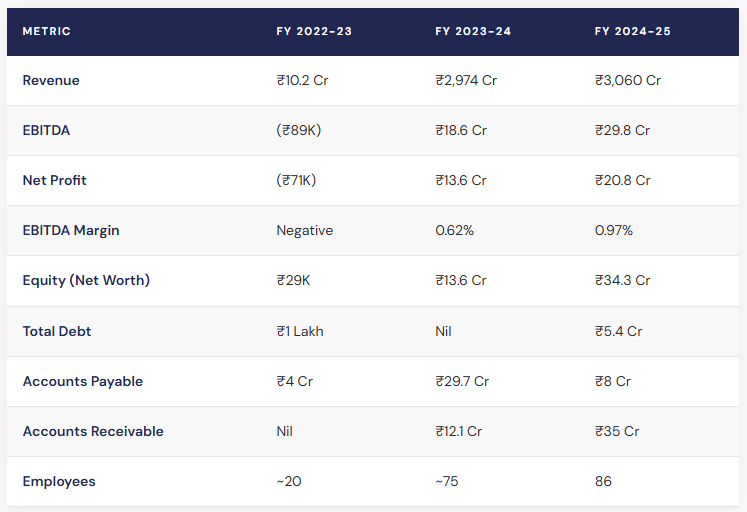

The revenue ramp: from ₹10 crore to ₹3,060 crore in 24 months

Tirupati Agrotech’s financial trajectory is extraordinary on its face. In FY2022-23, its first full fiscal year, it reported total revenue of ₹10.2 crore. In FY2023-24, that jumped to ₹2,974 crore. In FY2024-25, ₹3,060 crore.

A company with 86 employees generating ₹3,060 crore in revenue is clearly not a manufacturing entity, but a marketing and distribution entity. Tirupati Agrotech is the distribution arm for NK Proteins' manufactured products.

On margins, it is worth a note of context. Tirupati Agrotech’s EBITDA margin of under 1% reflects its nature as a pure distribution intermediary, the manufacturing margin sits with NK Proteins, where EBITDA runs at ~2.2%. For comparison, Adani Wilmar, one of India’s largest listed edible oil companies, operates at a similar 3 to 4% EBITDA margin. Thin margins in this sector are not a sign of a commodity play, they are the structural reality of a branded edible oil business.

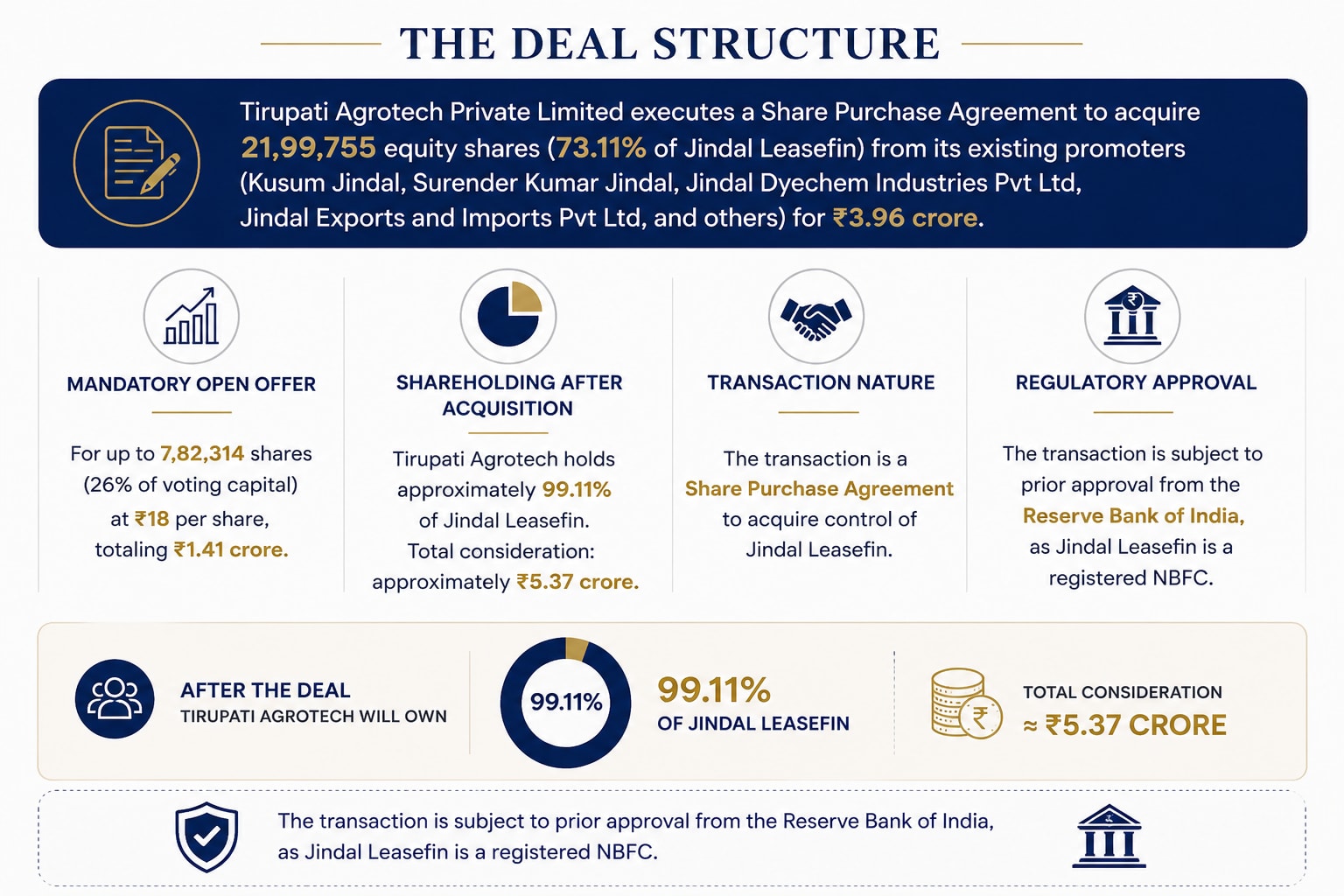

Jindal Leasefin: ₹5.37 crore buys a listed company

Jindal Leasefin Limited is registered with the RBI as a Non-Banking Financial Company, but in reality is one of the many shell companies listed on BSE.

A ₹3,060 crore revenue company paying ₹5.37 crore for a listed entity. No serious NBFC acquirer eliminates the public float to near-zero as a first move. The strategic motive here is not the NBFC. It is the listing.

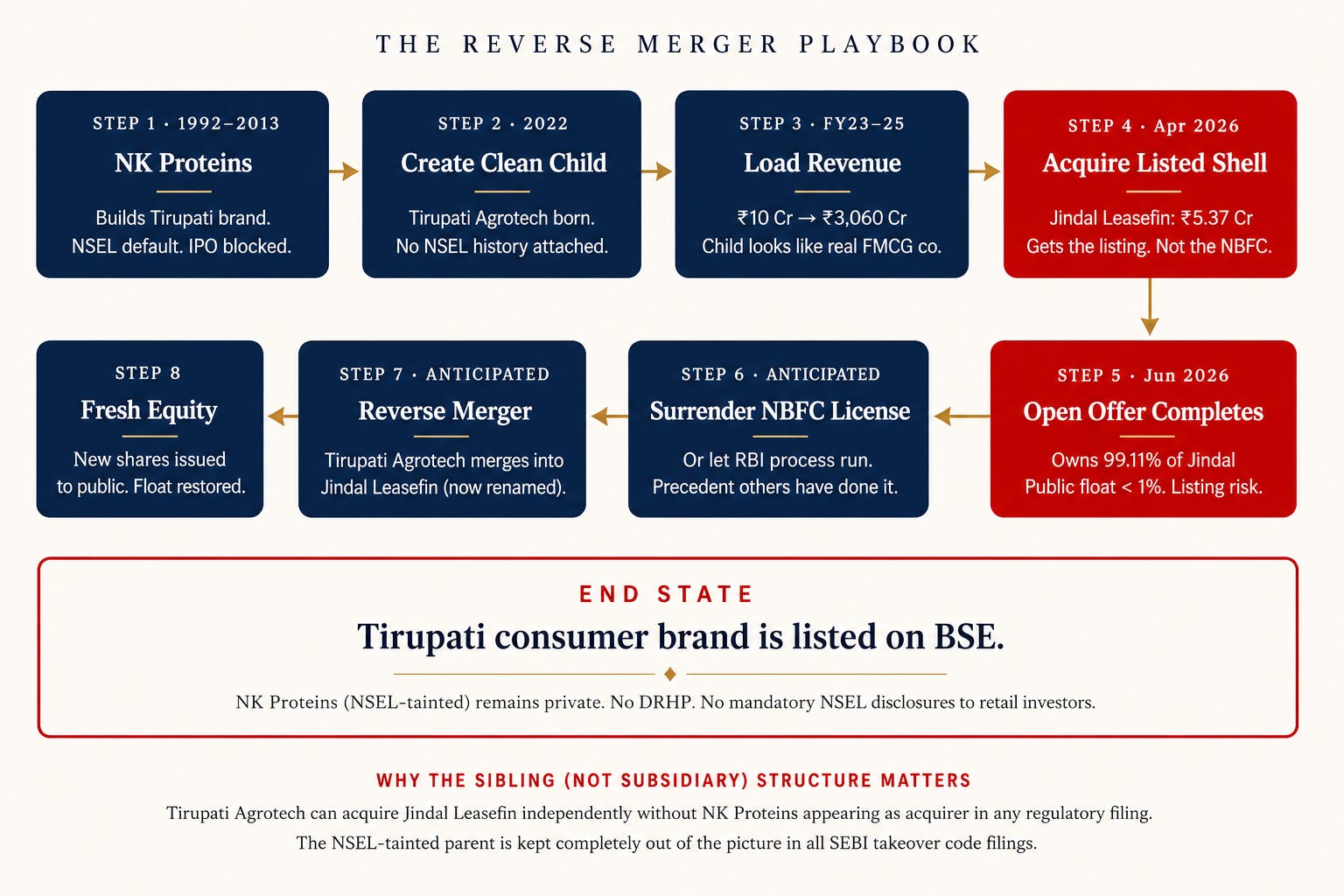

The reverse merger playbook, step by step

A reverse merger is a mechanism by which a private company acquires a public listed company (typically a shell or a dormant entity) and subsequently merges itself into the listed entity, effectively achieving a stock exchange listing without going through a conventional IPO.

The conventional IPO route requires the company to file a DRHP with SEBI, which mandates full disclosure of all material litigation, regulatory proceedings, and defaults. For NK Proteins or any directly associated entity, that document would require disclosure of the NSEL default of ₹970 crore, the MPID court proceedings, the ED attachment under PMLA, the outstanding liability to 13,000 investors, and the fact that the company’s founder was arrested in connection with one of India’s largest spot market frauds. No institutional investor would subscribe to that IPO. No investment bank of standing would underwrite it.

The reverse merger route, by contrast, avoids the DRHP entirely. Here is how the playbook likely unfolds:

Why the sibling structure was deliberate

This is where the legal architecture of NK Group becomes critical. Tirupati Agrotech and NK Proteins are group companies, not parent and subsidiary. In all SEBI Takeover Code filings related to the Jindal Leasefin acquisition, the acquirer is Tirupati Agrotech Private Limited. NK Proteins, despite being functionally the manufacturing backbone of the entire Tirupati brand operation, does not appear as an acquirer or in any capacity that would trigger NSEL disclosure requirements.

A subsidiary would create a consolidated entity structure that might require disclosure of the parent’s liabilities. A sibling company under common promoters operates independently. The structure achieves exactly this: the consumer brand revenue sits in a clean entity, the clean entity acquires the shell, and the NSEL-tainted parent is structurally isolated from the transaction.

The incorporation of Tirupati Agrotech just 3.5 years before this acquisition, with essentially no independent business before being loaded with ₹3,060 crore in group revenue, is the clearest evidence that this structure was purpose-built.

The question that remains

At its core, this appears to be a story of corporate separation.

NK Proteins has the operating history, the manufacturing backbone, and the Tirupati legacy. But it also carries the baggage of the NSEL crisis, including the Rs 970 Cr default, asset attachments, rating actions, and unresolved questions around investor recovery.

A conventional IPO would have forced this history into the open.

Tirupati Agrotech offers a cleaner wrapper. It is a newer entity, with a shorter record, a consumer-facing profile, and the ability to present the Tirupati story without carrying the full weight of NK Proteins’ past. The acquisition of Jindal Leasefin then potentially creates a route to public markets without the same level of IPO scrutiny.

That is why this is not just a listing story.

It is a governance story.

The business may be real. The brand may be strong. But the structure raises one uncomfortable question: is the group creating a cleaner platform for future growth, or a cleaner wrapper for an old past?

A brand can outlive a scandal.

But should a scandal disappear just because the brand survived?

IMPORTANT NOTE

We run a Smallcase called Asymmetric Growth — a curated portfolio built around one idea: find businesses where the upside is large and the downside is limited.

No noise. And yes, we use a bit of momentum where it works in our favour — but only to boost returns, never to chase them.

Just disciplined, research-backed investing.

If that sounds like your kind of portfolio, this is where you want to be.

If you know someone who’s tired of guessing and ready to invest with conviction, send this their way.

Explore our Newsletter Archive to catch up on previous editions.

😂Meme of the Week😂

🤝Connect with us

We’d also love to hear your thoughts and feedback on various platforms where we are active. Connect with us below:

Know more about Bastion Research @ Website,

Get daily updates from Bastion Research @ Twitter (X), @ WhatsApp Channel, @ LinkedIn and, @ Stocktwits

Watch insightful videos and company deep dive podcasts “Made in India” by Bastion Research @ YouTube

If you enjoyed reading this newsletter, please feel free to share it with others who might find it insightful.

Happy Investing!!!

Disclaimer: These insights are based on our observations and interpretations, which might not be complete or accurate. Bastion Research and its members may or may not have stakes in companies mentioned. This newsletter is for educational purposes only and is not intended to provide any kind of investment advice. Please conduct your own research and consult your financial advisor before making any investment decisions based on the information shared in this newsletter.